Pioneering new approaches to EITI reporting

A preliminary analysis of flexible EITI reporting shows improvements in the relevance, timeliness and cost-effectiveness of reporting.

The outbreak of COVID-19 has changed the context for EITI implementation across the globe. Implementing countries have had to contend with new realities. Traditional reporting and data collection practices have been hindered by budgetary constraints and health restrictions. Multi-stakeholder groups (MSGs) that relied on in-person fora for decision-making and trust-building have fewer touchpoints and have had to use virtual platforms to replace critical face-to-face meetings.

Like many organisations, the EITI has adapted to sustain its mission in the face of such obstacles. Recognising these challenges, the EITI Board agreed in May 2020 to introduce flexible measures allowing countries to deviate from the standard procedures of EITI reporting – namely the reconciliation of extractive company payments and government receipts – provided that EITI Reports disclose more timely and topical information that meets stakeholders’ needs for information. The EITI Board also extended a pilot project that seeks to explore alternative and more cost-effective approaches to reliable EITI disclosures.

Since then, almost a third of implementing countries have adapted their EITI reporting practices in some way. To date, 14 countries have published EITI Reports under the flexible format (with more expected in coming months), and a further two countries – Afghanistan and Germany – published reports as part of the pilot on alternative reporting.

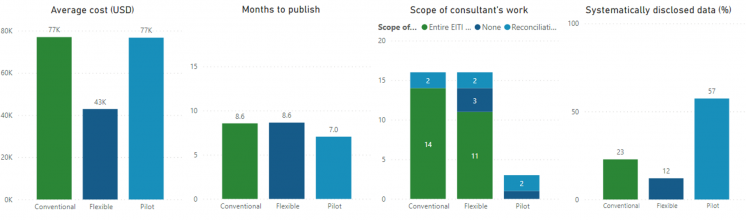

These approaches have created an opportunity for implementing countries to restructure their EITI reporting processes to build and extend systematic disclosures of EITI data, thereby integrating transparency into routine government and company systems. Progress on systematic disclosure, the default expectation for EITI reporting since 2016, has varied across countries. But flexible approaches have created space for implementing countries to re-engineer their reporting processes, and for the MSGs to play a leading role in overseeing disclosures.

While it’s important not to underplay the challenges of multi-stakeholder engagement through the pandemic, these pioneering examples have shown us that challenges can be seized as opportunities to spur innovation.

Improving relevance and timeliness

Implementing countries have used new approaches to reporting to improve the relevance of EITI disclosures by including more current information. Three-quarters of countries included information on the impact of COVID-19 on extractive industries, and Ghana published a dedicated thematic report on the effects of the pandemic. More than two-thirds of countries that adopted flexible reporting have presented forward-looking analysis of their extractive sectors, with projections for future production, exports and government revenues.

Flexible reporting has also led to a number of innovations and first-time disclosures, including on issues related to the energy transition in Germany and the Philippines, environmental management in Afghanistan, anti-corruption efforts in Indonesia and Germany, informal extractive activities in Afghanistan and Mauritania and gender aspects of the extractive sector in Ghana, Guatemala and the Philippines. While innovations are not exclusive to flexible EITI reporting, with a number of conventional EITI Reports also covering topical issues such as the impact of COVID-19, they do seem to have been accelerated through this approach.

The timeliness of data produced under the flexible reporting format improved in some countries. On average, flexible EITI Reports have had a 16-month time lag between the financial data reported and the date of publication, compared to a lag of 18 to 24 months for conventional EITI Reports. Seven countries are ahead of their reporting schedule with data for the 2020 fiscal year already published, including Honduras and Malawi which participated in flexible reporting. Eighteen countries have yet to publish data for 2019 fiscal period, most of which are undertaking conventional reporting.

Reducing cost and resources

EITI Reports that adopted the flexible approach were more cost-effective than conventional reconciliation reports. On average, costs dropped from USD 77,000 for conventional reports to USD 43,000 for “flexible” EITI Reports, reducing expenses by 44%. Some countries, such as Afghanistan and Zambia, did not procure Independent Administrators to produce EITI Reports, instead drawing on the resources of multi-stakeholder groups and national secretariats.

This may have had an opportunity-cost however, as EITI stakeholders devoted more attention to the details of reporting than to other key activities such as outreach, dissemination and implementation of recommendations for reform. It is also worth noting that expenses ranged significantly across countries – while Mongolia reduced its reporting costs from USD 42,000 to USD 17,300, those of the Philippines’ increased from USD 40,000 to USD 46,800.

While it was expected that the time to produce “flexible” EITI Reports would decrease (and thereby free resources for analysis and dissemination of data), this varied considerably. Ten countries did produce reports more efficiently – Chad stands out having reduced its reporting cycle from 12 to 3.5 months. Other countries remained constant or increased the duration of their reporting cycle.

Maintaining quality and comprehensiveness

On average, flexible reports covered more companies with data on their payments to governments. However, countries that have taxpayer confidentiality laws saw a slight decline in the comprehensiveness of government revenues – on average, 82% of government revenues were disaggregated in flexible reports, compared to 88% in conventional reports.

Nonetheless, the transition from conventional to flexible and pilot alternative approaches to EITI reporting has not resulted in a deterioration in the reliability of financial data related to company payments and/or government revenues, as assessed by MSGs. However, MSGs’ greater involvement in the reporting process may have affected the impartiality of this assessment, and it is worth noting that these assessments were not based on a detailed review of statutory procedures or practices in government audits and assurances of government revenues.

EITI reporting has been a central feature of the EITI since its inception. The scope of reporting has evolved considerably over time, and countries are increasingly disclosing data systematically. Nonetheless, reporting has proved to be an expensive and cumbersome exercise for many implementing countries. The early adopters of flexible and alternative reporting provide valuable learnings for countries who are seeking to take on more cost-effective and efficient solutions for EITI reporting, without compromising on the quality and relevance of disclosures. They also offer important lessons as the EITI Board reviews the efficacy of EITI reporting and considers future parameters for EITI implementation.

Countries that participated in flexible EITI reporting include Argentina, Chad, Democratic Republic of the Congo, Ghana, Guatemala, Guinea, Honduras, Indonesia, Liberia, Madagascar, Malawi, Mauritania, Mexico, Mongolia, Philippines, Sierra Leone and Zambia, and Guinea, Madagascar and Mexico are in the process of preparing reports under this format. Afghanistan and Germany participated in the pilot on alternative approaches to reporting, which Mauritania joined in 2022.

Related content